Greythorn Fortnightly Newsletter - Issue #6

Crypto Market Insights by the Greythorn Research Team. Detailing technical levels, option flow, and an exploration into cash-flow generation across DeFi & value accruals in the ETH Post-Merge space.

Crypto Market Insights

Market Summary

Bitcoin & Ethereum are up 2.76% & 11.32%, respectively, over the past fortnight.

The Goerli testnet successfully merged on the 11th of August, setting up mid-September for the final stage of the Merge.

The U.S. Treasury has banned the usage of the crypto-mixing service Tornado Cash.

US CPI came in lower than expected. 8.5% vs 8.7% est.

Traditional markets, the S&P 500 & Nasdaq 100, are up 4.49% & 6.13%, respectively, over the past fortnight.

Greythorn views that Bitcoin will remain between $21,000 & $27,000 for this week.

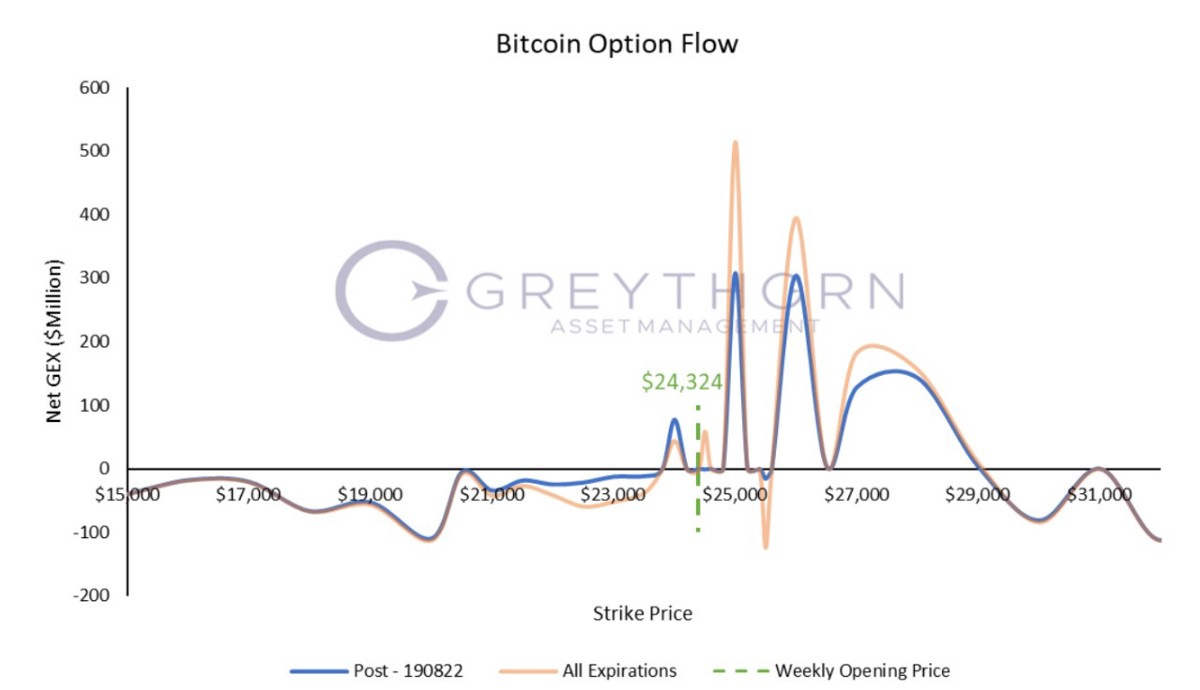

Greythorn Option Flow Model

Bitcoin has increased 2.76% over the past fortnight and is currently trading at ~$23,900.

Increased volatility is expected at a series of price levels with negative net GEX, namely the interval between $15,000 and $23,000, $25,500, $30,000 and $32,000.

There are very few significant support levels from the graph above, with $24,000 and $21,000 as the only two relatively weak support levels. As the market approaches the 19/08 weekly expiration, $24,500 is expected to become another weak support/resistance.

In contrast, several strong resistances can be observed. $25,000 is the first significant resistance level, followed by $26,000 and $27,000 as the second and the third resistance levels, as suggested by the considerable option supply at these prices.

Net GEX for this week is 2.5x that of the previous fortnight, indicating a flatter market with more liquidity and lower crash risk. The graph also displays that the magnitude of positive GEXs at $25,000, $26,000 and $27,000 is remarkably greater than any of the negative GEX levels. Thus, much of the current positioning across options markets is providing liquidity rather than taking it.

Greythorn believes that Bitcoin will range between $21,000 and $27,000 over the upcoming week based on our option flow model.

For an introduction to Greythorn Option Flow Model, please refer to our newsletter from 8th June 2022 here.

Core Research: dPerps and Real Yield

The ever-changing landscape of DeFi has cycled from its early innovative years spear-headed by the likes of AAVE, UNI and COMP to food tokens attracting billions of dollars into a burgeoning eco-system. Rife with highly experimental and untested platforms, culminating in the liquidation of many institutions throughout the industry due to over-exposure and over-reliance on DeFi and leverage.

With The Ethereum Merge kicking off, two major crypto narratives have started to pick up steam, namely;

1. Ethereum’s Merge narrative and distributed ledger technology projects that benefit from the switch.

2. DLT projects accrue more positive cash flow to its holders than inflationary emissions. They pay out such revenues in stables or blue-chip cryptocurrencies.

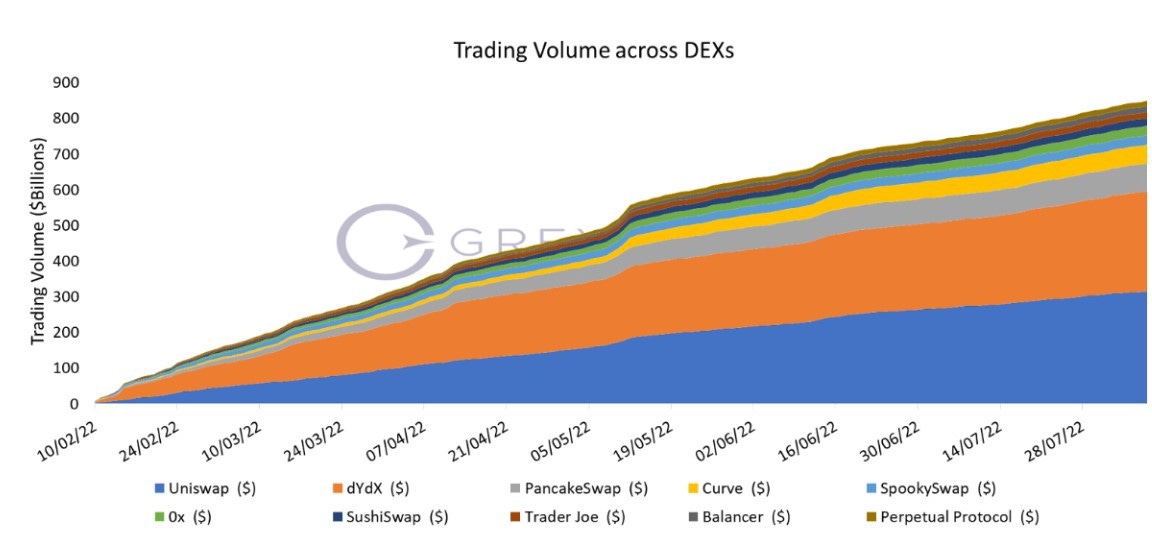

As we approach the merge, we find a considerable influx of trading volume in the DEX space, with $UNI leading the charge and $dYdX coming in second in trading volume.

Now that it’s #RealYield season, this fortnight’s piece will be delving into the various DLT projects and compare revenues along with valuations of a few prominent decentralised perpetual exchanges that readers should consider analysing as we come closer to the ETH merge.

Most leveraged trading occurs through popular centralised platforms that provide the best UX and UI. The question then arises, what are the benefits of decentralised trading platforms?

The main benefits and factors are the same as for most dApps:

Self-custody of funds: Trading funds are not in custody by any centralised party, eliminating the risk of centralised control of user funds.

Lack of KYC: By trading on decentralised exchanges, users do not require to pass any KYC/AML requirements, and the barrier to entering is the balance in their digital wallets and their choice of DEXs.

Better Uptime: Due to being hosted as a smart contract on the blockchain, any DEX platform would benefit from a blockchain’s ability to stay online at all times. This is a significant advantage as centralised exchanges have historically shown to have untimely issues during periods of increased volatility and trading volume whilst dApps continue to perform consistently during the same timeframe.

The second quarter of 2022 has brought market uncertainty, dwindling interest in the ecosystem, and myriad repercussions in the market. Despite the turmoil in cryptocurrency and traditional asset classes, users would still trade and invest.

Users will still come despite the market cycles, and investors may still be able to profit through their activities on trading platforms. This source of demand is the prime driver of any trading platform. Whether trades are placed directionally or not, an investor could profit by investing in tokens related to said trading platforms.

Hence, we will compare three tokens within said space, namely $dYdX, $GMX, and $GNS.

To read the whole article, please click here to view the full PDF.